Six Quarters of the Same Discount: Shettigere Has Appreciated 14% a Year Without Closing the Gap to Hebbal

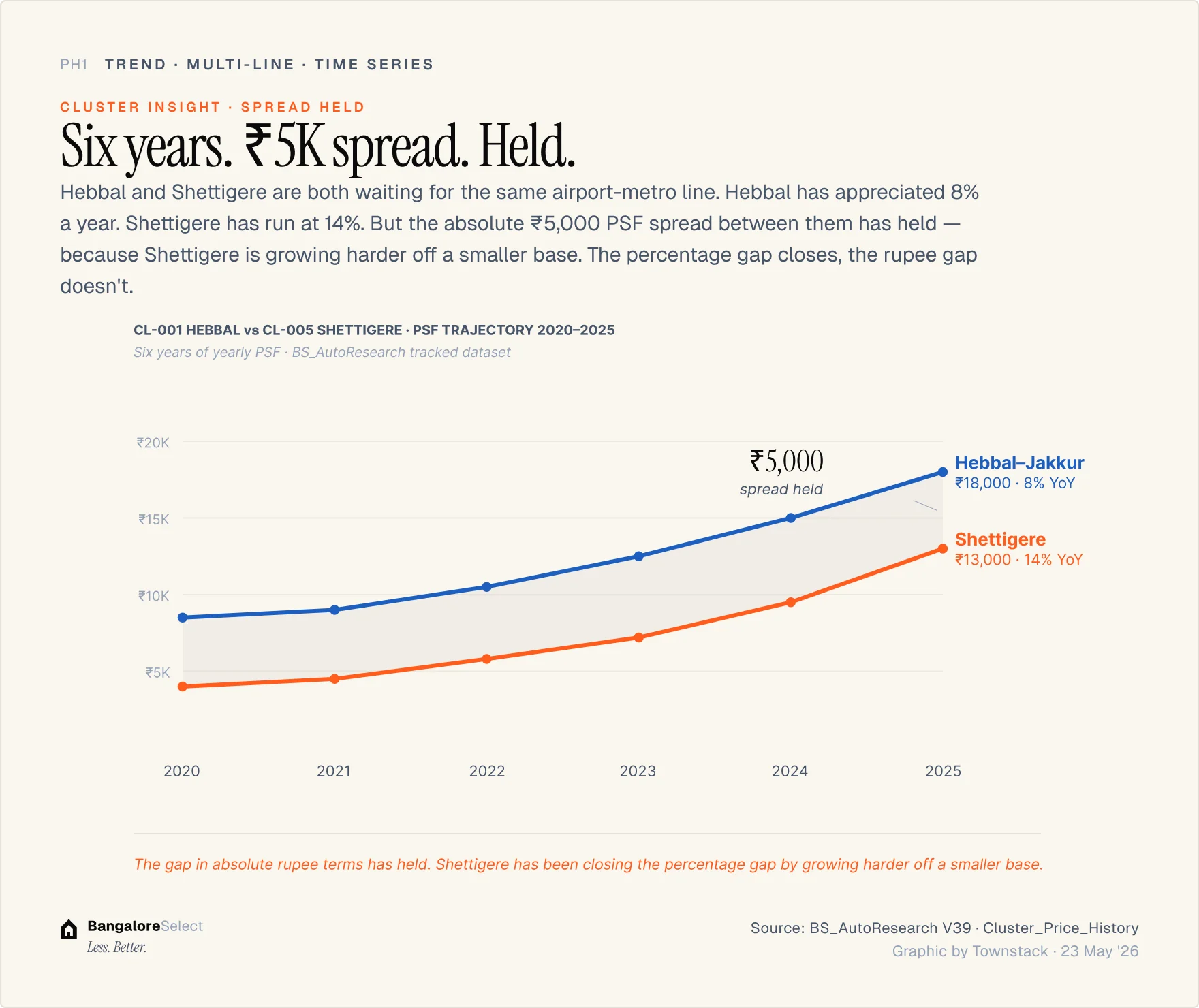

Shettigere has the highest north Bengaluru appreciation rate at 14 percent YoY but still trades at ₹13,000 psf, 28 percent below Hebbal, because Hebbal is also moving. Six quarters of compounding 14 percent gains have closed the gap arithmetically while supply expansion at Birla Trimaya and Tata Varnam keeps the spread structurally open.

If you've sat through a North Bangalore real-estate sales pitch any time in the last three years, you've heard a version of the same line. Buy now, before the metro arrives. The 30-kilometre stretch of NH-44 between Hebbal Junction and Kempegowda International Airport, six residential clusters strung along it, every one pinned to the Bangalore Metro's Phase 2B opening, has been selling that line since BMRCL filed Phase 2B for Cabinet approval. The line works because the metro is real. What the pitch doesn't explain is why the cluster furthest from the city, Shettigere, has been outpacing the one nearest to it, Hebbal-Jakkur, for six straight quarters without closing the price gap between them.

₹13,000 a square foot in Shettigere. ₹18,000 in Hebbal-Jakkur. Both clusters wait for the same line. The cheaper one has appreciated 14 percent a year. The expensive one, 8 percent. The spread between them, ₹5,000 psf, or 38 percent, has not moved.

Two reads on why. Both are rational. Neither has been falsified yet, because both predict what's already happened.

What ₹13,000 psf is actually pricing

Take the catalyst inventory first. BMRCL's Phase 2B Blue Line terminates within four kilometres of the Shettigere centroid. The Satellite Town Ring Road, Karnataka's outer-outer loop around Bangalore, still under construction in patches, passes through. NHAI awarded the Sadahalli Underpass contract in January 2026 with a target completion of April 2027 (April 2027 in the NHAI calendar; somewhere closer to 2028 in the calendar of things that actually finish on Bangalore's airport road). And the airport's ground-side employment catchment, Boeing's engineering centre, SAP Labs's second campus, Collins Aerospace, Foxconn's Precision Engineering facility, the dual-airline MRO hub, overlaps the cluster boundary.

Four corridor-defining infrastructure events, nominally landing in the same 18-month window. The 'nominally' matters. BMRCL's Phase 2B opening window is officially May to November 2027. The November is doing some work in that sentence. Anyone who has watched a Bangalore underpass go from contract award to ribbon-cutting will reach for a slightly larger range on the underpass too. None of which makes the catalysts unreal. It just means the timing question is open in a way the project glossies don't quite admit.

Underneath the timing question is a market that's already moved. Phase 4 at Birla Trimaya cleared ₹650 crore in Q1 2026 bookings. Tata Varnam reportedly sold ₹1,000 crore in 60 days at launch, if that holds up under later disclosure, Shettigere is the airport-corridor cluster that absorbed the most in early 2026. New 2 and 3 BHK rentals at Birla start around ₹35,000 a month; 4 BHK lake-frontage at ₹65,000. This is what pricing looks like when buyers have already concluded that the timing question is a when, not an if.

The conventional read

The gap closes after the metro opens.

Logic runs mechanical. Shettigere trades at a metro-pending discount. When Phase 2B's airport-side leg comes online, call it 2027, call it 2028 if you're being honest with yourself about Bangalore infra dates, the discount thins. Pricing converges toward Hebbal-Jakkur's ₹18,000. The residual gap reflects Hebbal's earlier maturity and the Hebbal Junction multimodal hub. The ₹5,000 spread compresses to ₹2,000 or ₹3,000 within 24 months of revenue service.

It's a reasonable read. The mechanics are visible in other Indian metro stories. Whitefield repriced after Purple Line revenue service. Mumbai's western corridor moved on Line 7. Shettigere has more concentrated catalyst density than either, and a smaller starting base to grow from. If this read is correct, this is the cluster that runs hardest in the 24 months after Phase 2B opens.

The contrarian read

The metro arrives. The spread holds.

Hebbal's premium is structural. Manyata Tech Park sits four kilometres east of the cluster. The Embassy Manyata Commonwealth Bank of Australia built-to-suit locks 1.4 million square feet of GCC space from Q4 2026, and 'locks' is the right verb, because a built-to-suit means Hebbal has GCC tenants the way KIADB has aerospace tenants. The Hebbal Junction multimodal plan, the Hebbal-Mekhri double-deck tunnel announced in the March 2026 Karnataka Budget, the existing flyover loop already delivering 20 to 30 percent junction relief, Hebbal sits on infrastructure depth that doesn't transfer to Shettigere just because the two clusters share a metro line.

Under this read, the metro is necessary for Shettigere's appreciation but not sufficient to close the structural premium. The gap holds at 30 percent. Shettigere keeps outpacing Hebbal in YoY terms because it's starting from a smaller base. The absolute spread persists because the underlying differentiation persists.

Both reads are internally consistent. Both predict what the last six quarters showed. The cluster appreciated. The gap held.

The two clocks running underneath

The conventional read needs Phase 2B's airport-side leg to actually open in something resembling its window. It also needs the Hebbal-end of the same package, which the December 2025 Revenue Minister site inspection found at 0.02 percent track work, a number that sits firmly in the 'someone counted carefully' category, to not slip so badly that the cluster terminus opens to no through-running service for two years.

The contrarian read needs one thing only. Manyata occupancy depth keeps compounding through 2027 in a way the Shettigere employment catchment cannot replicate. The CBA tenant lock is the leading signal. If Embassy Manyata's Phase 2A million sqft expansion fills out as expected, the GCC depth at Hebbal becomes increasingly difficult to substitute. The premium then has a tenant base that doesn't migrate.

The two reads aren't symmetric. One is a delivery-timeline bet on something Bangalore is famously inconsistent at. The other is a structural-tenant bet on something Bangalore is famously consistent at.

The supply variable nobody flags

Birla Trimaya Phase 4 adds roughly 550 units. Tata Varnam Phase 1 adds 583. About 1,130 active pipeline units launching on the same road in the same year, with Sattva City on the cluster's western edge in CL-004 Sadahalli contributing additional pressure.

If absorption rates hold, the cluster carries the appreciation through to metro opening. If they thin, and the broader North Bangalore RERA launch wave of 37,103 units in 2025 is a credible reason to expect some thinning, pricing power compresses on both projects simultaneously. Phase 2 launches at either developer become the visible absorption proof point. Buyers entering Phase 1 at ₹13,000 psf should size for the possibility that Phase 2 prices at a premium they captured, or at a flat number they did not.

The Sunday at Trimaya

On a Sunday morning in April, the wait to walk Birla Trimaya's Phase 4 ran about an hour. The buyer profile in that queue wasn't speculator-flat. It was mixed, a couple of KIADB-based engineers extending their range, a returning NRI running an in-laws-house-too errand on the side, two families comparing notes on Harrow versus Stonehill. The conversations were about possession dates and floor-plate fenestration. They were not about whether to buy. That decision had already been made somewhere upstream.

The cluster's social fabric is still arriving. Reliable retail thins out past the Birla site office. Schools that aren't Harrow ask for a 30-minute commute. Monsoon hits Devanahalli differently from south Bangalore, and any first-time site visit between June and September should include a back-road test drive before committing. None of this contradicts the appreciation thesis. It just means the lived-in experience is two years behind the pricing, which is the part the brochure understandably doesn't lead with.

This is what a 14 percent YoY cluster looks like at ground level. Not a queue of hot money. A queue of people who've already absorbed the timing question and concluded the answer is good enough. Whether they're right is a question for 2028. The market today is the market they've made.

The cluster has held the discount for six quarters. The next six are the ones that count.

Sources. BangaloreSelect Tracked Dataset (BS_AutoResearch W3 22-MAY-2026). BMRCL Phase 2B construction inspection: Deccan Herald, December 2025. NHAI Sadahalli Underpass award: Bengaluru Airport Road / NHAI, January 2026. Embassy Manyata CBA built-to-suit: Embassy REIT investor disclosure. Hebbal-Mekhri double-deck tunnel: Karnataka Budget March 2026.

The Sunday at Trimaya

On a Sunday morning in April, the wait to walk Birla Trimaya's Phase 4 ran about an hour. The buyer profile in that queue wasn't speculator-flat. It was mixed, a couple of KIADB-based engineers extending their range, a returning NRI running an in-laws-house-too errand on the side, two families comparing notes on Harrow versus Stonehill. The conversations were about possession dates and floor-plate fenestration. They were not about whether to buy. That decision had already been made somewhere upstream.

The cluster's social fabric is still arriving. Reliable retail thins out past the Birla site office. Schools that aren't Harrow ask for a 30-minute commute. Monsoon hits Devanahalli differently from south Bangalore, and any first-time site visit between June and September should include a back-road test drive before committing. None of this contradicts the appreciation thesis. It just means the lived-in experience is two years behind the pricing, which is the part the brochure understandably doesn't lead with.

This is what a 14 percent YoY cluster looks like at ground level. Not a queue of hot money. A queue of people who've already absorbed the timing question and concluded the answer is good enough. Whether they're right is a question for 2028. The market today is the market they've made.

The cluster has held the discount for six quarters. The next six are the ones that count.

Read more on the Shettigere cluster page for the live project list, trigger feed, and price-history chart referenced in this article.